The Boomer Economy: When “Over 65” Becomes an Economic Class

For many younger Americans, this doesn’t feel like an economy. It feels like a waiting room.

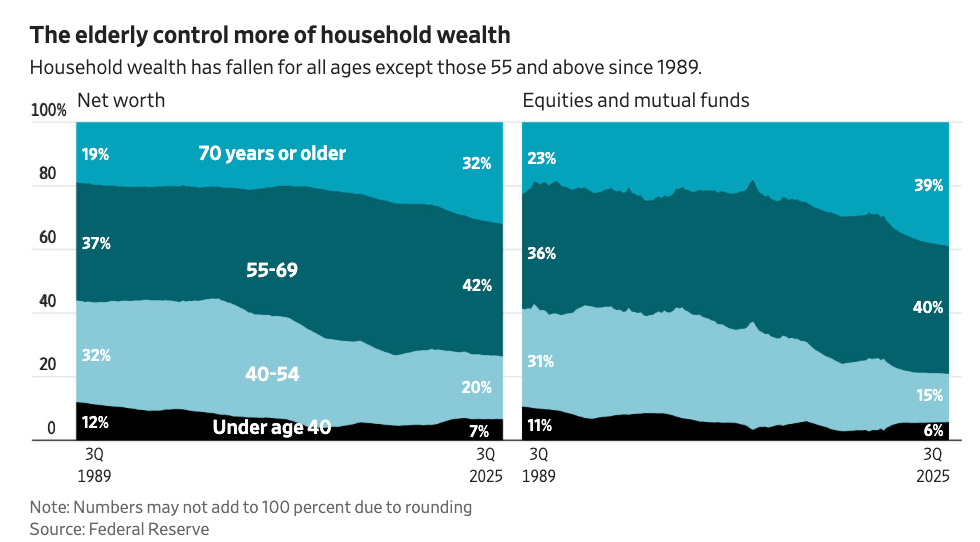

Two-thirds of Zoomers struggle to afford their rent or mortgage. Meanwhile, Americans over 70 control nearly a third of all household wealth in this country, up from a fifth just two decades ago. Those two facts exist in the same economy and they aren’t coincidental. They are the predictable result of decades of policy choices that funnel resources upward by age.

This isn’t just about older people having more time to save. This is a story about an entire economic structure -tax policy, federal spending, housing rules, and asset inflation- that has been engineered, consciously or not, to enrich retirees while leaving younger Americans to figure it out on their own.

And as the Wall Street Journal’s Greg Ip put it this month: there has never been a better time in America to be old. The rest of us? Not so much.

The Spending Gap No One Wants to Talk About

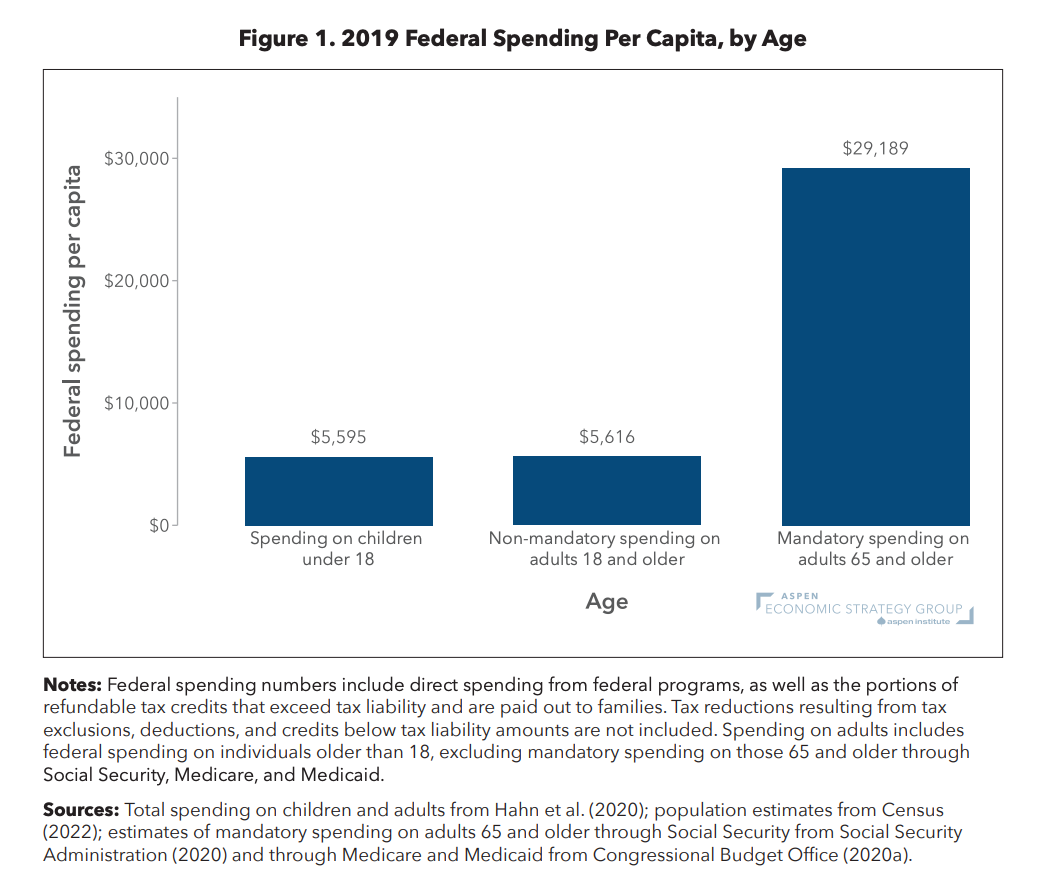

Now look at how the federal government allocates resources by generation. In 2019, the federal government spent over $29,000 per person aged 65 and over through Social Security, Medicare, and military and civil service retirement compared to roughly $5,600 per child under 18.

That’s a ratio of more than 5 to 1, according to economists Melissa Kearney and Luke Pardue of the Aspen Economic Strategy Group.

And it’s bipartisan. In 2022, veterans’ benefits were expanded at a 10-year cost of $277 billion. In 2024, Social Security coverage was extended to certain municipal employees at a cost of nearly $200 billion over a decade. Last year’s OBBB carved out a new $6,000 tax deduction specifically for people 65 and over. Federal spending on elderly programs has climbed from 6.9% of GDP in 2007 to 9.4% last year, and the Congressional Budget Office projects 11.3% by the mid-2030s.

Social Security is one of the most effective anti-poverty programs in American history. Without it, more than 37% of older adults would fall below the poverty line, according to the Center on Budget and Policy Priorities. That’s a legacy worth defending. But the overall balance of public investment deserves scrutiny too. The child poverty rate in 2024 was 14.3%. For adults 65 and over, it was lower and has been since 1974. We solved elderly poverty by making it a political priority. We never did the same for kids.

Only The Few Can Own

The wealth gap shows up most viscerally in housing.

Nearly 80% of Americans 65 and over own their homes, a rate that has held steady for two decades even as homeownership has declined for those aged 35 to 64. Baby boomers sit at a 79.9% homeownership rate as of 2025. Gen Z? Just 27.1%, per Redfin. And while that’s up slightly from 26.1% the year prior, it’s hardly a breakthrough as Redfin senior economist Asad Khan noted, young people are making gains because they’re making sacrifices, not because homes suddenly became affordable.

A Redfin survey from November 2025 puts the human cost in sharp relief: 67% of Gen Zers report struggling to afford rent or mortgage payments. Among those who struggle, 18% have skipped meals entirely, 20% have sold belongings, 15% have moved back in with their parents, and 6% have delayed having children. Homebuyers today need to earn about $111,000 a year to afford the typical U.S. home roughly $25,000 more than the median household income.

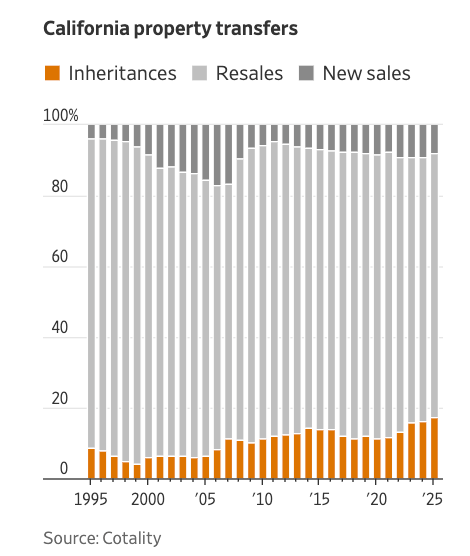

And in California, the distortions are extreme enough to constitute their own cautionary tale. The Wall Street Journal reported this past week that 18% of all property transfers in the state last year nearly 60,000 homes occurred through inheritance.

That’s a record going back to 1995 and roughly double the national rate. Inheritance has become less of a windfall and more of a housing strategy.

The mechanics are straightforward. Proposition 13, passed in 1978, caps annual property-tax increases at 2% based on a home’s original purchase price, rather than its current market value. That means someone who bought a house decades ago pays taxes on a much lower assessed value, while a new buyer’s tax bill resets to today’s far higher price. A new buyer today can pay 10 times more in property taxes than a longtime neighbor in an identical home. On top of that, the federal stepped-up basis rule resets a home’s tax value at death, allowing heirs to avoid enormous capital-gains bills on decades of appreciation. The result is a system where homeowners have every financial incentive to hold until they die, choking supply, inflating prices, and turning ownership into something younger Californians can only access through their parents’ mortality.

The Worker Shortage Nobody Mentions

There’s another dimension to this that doesn’t get enough attention.Labor force participation for Americans 65 and over had been gradually ticking upward for years. Then COVID hit. Participation plunged for every age group but rebounded for everyone under 65. For those 65 and over, it hasn’t come back. Combined with plummeting immigration which historically supplements the working-age population we’re heading into a period where a smaller share of Americans will be producing what a growing share of retirees consume.

That’s a fiscal problem, an inflation problem, a growth problem, and a political problem all at once because the people bearing the burden of that production are the same ones locked out of homeownership, saddled with student debt, and watching the federal budget prioritize a generation that’s already the wealthiest in American history.

What Democrats Should Do About It

Here’s where I land: the cost-of-living crisis young voters feel is structural. The economy is organized to protect the wealth of people who already have it, and the policy toolkit from Prop 13 to the stepped-up basis to the sheer scale of elderly entitlement spending reinforces that tilt every year.

Democrats should:

Reform housing policy to work for all age groups. Prop 13-style property tax structures, expanding capital-gains exclusions to incentivize older homeowners to sell rather than hold until death, and pushing zoning reform that allows new construction at scale. As I’ve argued before, allowing mixed-use development, eliminating parking mandates, and expanding ADUs can meaningfully expand supply if the political will exists to overcome the NIMBY coalition that skews older and wealthier.

Rebalance public investment toward younger generations. The 5-to-1 federal spending ratio between elderly and children is a choice, not a law of nature. Evidence-based investments in children early education, child tax credits, healthcare access yield high social returns. The research is clear; what’s missing is the political commitment to act on it.

Be honest about Social Security’s future. By 2032, the program won’t be able to pay full benefits. Fixing it will require some combination of higher taxes or adjusted future benefits cuts that will fall largely on today’s workers. Pretending otherwise isn’t compassion. It’s cowardice, and younger voters know it.

Frame all of this as a cost-of-living issue. The affordability crisis has a generational dimension, and voters under 45 feel it acutely. Democrats who can credibly articulate why the economy feels rigged and offer structural solutions, not just sympathy, have a winning message for 2026.

The Bottom Line

The system of rules, incentives, and spending priorities that governs this economy has drifted dramatically in one direction over the past four decades. The policies that enabled one generation to buy homes for $150,000 and watch them appreciate to $1.8 million while simultaneously blocking new construction, underfunding children, and loading the federal budget toward retirees are choices that can be revisited.

The question for Democrats is whether they’re willing to have that conversation, especially when many of their most reliable voters are the ones benefiting from the status quo. As I wrote last year: boomers love progress — until it moves next door. The question is whether Democrats have the nerve to ring the doorbell anyway.