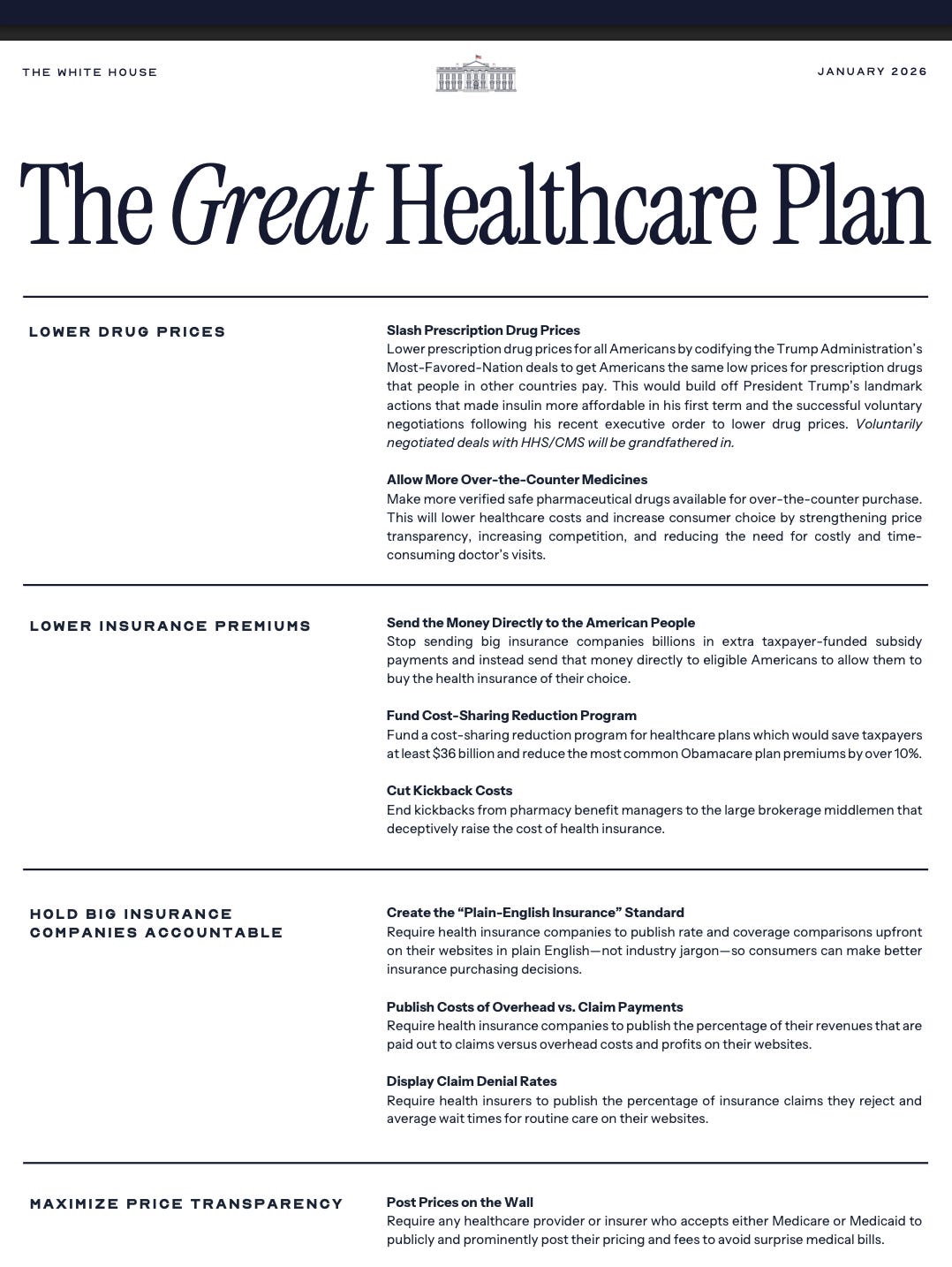

New “Concepts of a Plan” Dropped

Trump unveiled what the White House is calling The Great Healthcare Plan recently urging Congress to “enact” this comprehensive framework to lower drug prices, reduce insurance premiums, and “hold big insurance companies accountable”.

Image Credit: The White House

At first glance, this framework reads like a grab-bag of populist-sounding healthcare ideas – some of which borrow from existing ACA provisions (insurer transparency rules and plain-language coverage summaries already exist in the ACA) and others that are longtime Republican favorites (health savings accounts and deregulation). What’s striking but not surprising, however, is how light on specifics the plan is. The White House document spans only two pages, offering lofty objectives but absolutely no detail on how to achieve them, as health policy analysts have pointed out. For example, it promises to “send money directly” to people for premiums – but via what mechanism? New tax credits? Expanded HSAs? And how much money, and to whom? Those details are nowhere to be found.

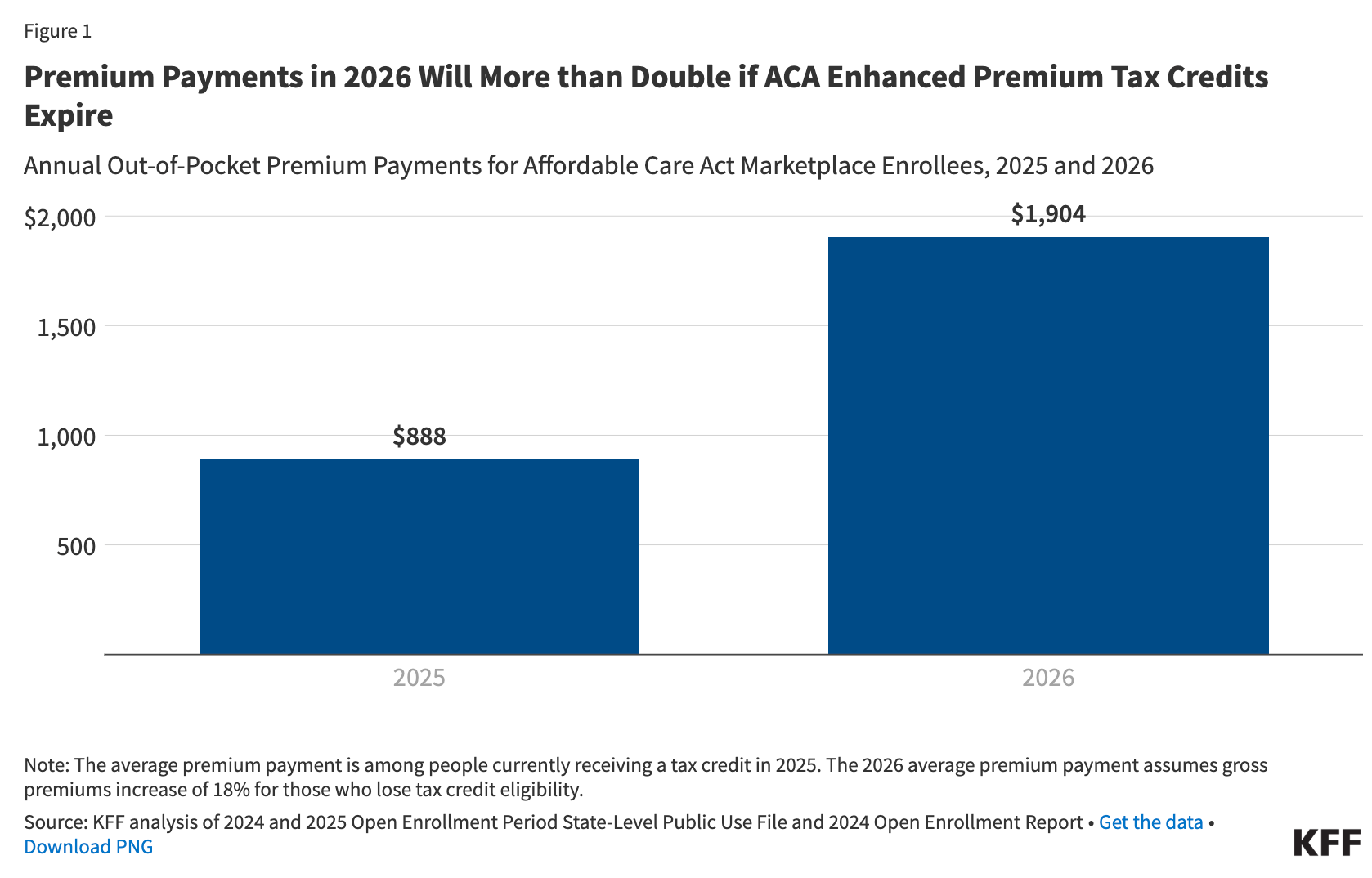

And yet 22 million Americans just saw their health insurance premiums jump in 2026 when enhanced subsidies expired. A family of four earning $45,000 faces a ~$1,600 annual increase, average premiums this year are set to more than double. Trump’s plan doesn’t restore that help. And if it destabilizes insurance markets as the Congressional Budget Office warns, costs could spiral even higher as healthier people drop coverage and premiums jump another 4-7% for those who remain. Higher costs are voters’ main triggers, and this expiration leads to one of the biggest hits in a family’s household budget.

Image Credit: KFF

The plan pointedly does not commit to restoring the enhanced ACA subsidies that expired at the end of 2025. Those temporary subsidies (first expanded under Biden) had capped marketplace premiums for millions of Americans. Rather than simply extend those subsidies, Trump’s framework criticizes them as “extra taxpayer-funded payments” to insurers and suggests rerouting that money to individuals’ health accounts. This is a huge pivot with potentially huge consequences: health economists warn that if you yank support out of the ACA exchanges and instead give people cash (especially without strong rules), you risk destabilizing insurance markets.

In short, Trump’s “great” plan seems to offer more buzzwords than solutions. It focuses heavily on cost-cutting measures but doesn’t clearly answer the biggest healthcare question of the past decade: what to do about coverage and affordability for the millions who rely on Obamacare. Even supporters concede the plan is more a “framework” than fleshed-out policy. And crucially, most of its major changes would require Congress to act, which is hardly guaranteed even with slim GOP majorities.

More Smoke and Mirrors? Timing and Political Context

Given this history, it’s hard not to view Trump’s big healthcare announcement with a dose of skepticism. Why now? The timing coincides with a number of other challenges and controversies swirling in Trump’s world – leading some observers to wonder if the Great Healthcare Plan is meant to change the subject and mollify voters, rather than actually solve healthcare woes.

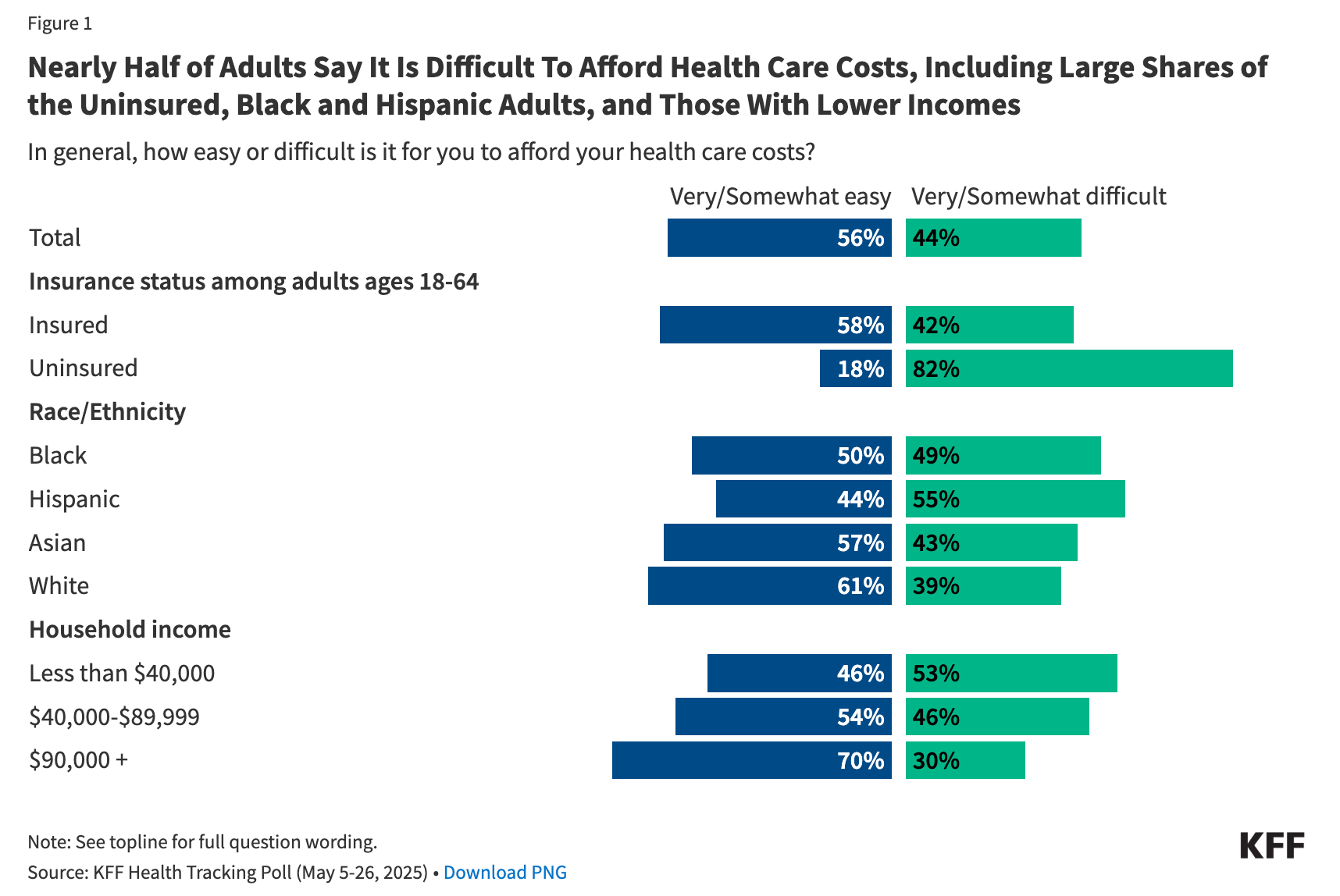

Given these concurrent dramas – roiling markets and allies with tariffs, alarming Europe with Greenland land-grab schemes, and igniting protests regarding ICE – it’s not far-fetched to think Trump’s sudden focus on a new healthcare plan is, at least in part, a political maneuver to regain control of the narrative. Being able to afford healthcare remains a top concern for American families year after year. Image Credit: KFF

If Trump can go on the offensive about lowering drug prices and helping “you and your pocketbook,” he might shift some attention away from the more controversial stories dominating the news.

So is this Great Healthcare Plan truly great? I’m not convinced. Even the name feels like an echo of past grandiose promises – remember Trump’s “phenomenal” healthcare plan that was always coming in two weeks? We’ve yet to see anything concrete materialize from those words. After DECADES of Republicans attempting to put a plan together and recent years of Trump’s continual assurances that a credible replacement was imminent, it simply never came. In essence, the more things change, the more they stay the same: Republicans still talk about replacing Obamacare, Trump still insists he has a beautiful plan, and yet the substantive policy either doesn’t exist or can’t get enacted.

Ultimately, though, the lack of detail and the historical track record suggest this plan may be more of a political prop than a policy breakthrough. It faces an uncertain path in Congress, lukewarm reception from health experts, and deep skepticism from the public – many of whom remember 2017 and do not want another round of repeal chaos. Compared to 2017, the United States is older, sicker, and far more dependent on the health care system, while also carrying significantly more federal debt. That reality makes unserious, Mad Lib–style health policy more dangerous, not less.

Voters have made clear they want tangible relief: lower costs, less complexity, an easier life. This plan delivers none of that. The American public has been clear for years that they want lower premiums and stable coverage. This plan suggests Republicans still don’t share that urgency.

You can’t fix American healthcare with slogans, and so far slogans are mostly what we’ve got. Trump’s Great Healthcare Plan may be new in name, but it remains to be seen whether it’s anything more than the latest chapter in the GOP’s long, unfinished (and perhaps unfinishable) quest to replace Obamacare with “something terrific.” In the meantime, consider this: if this plan doesn’t pan out, we might just find ourselves two weeks away from yet another great plan – and another after that – as the cycle continues.

If and when the direct-to-insurer subsidies are replaced with a cash handout to individuals, two things will happen:

1) The people will pocket the money and stop buying insurance.

2) When they get sick or injured, they will go to the hospital and claim hardship. Their bills will be written off.

I see this, literally, every day. If someone is uninsured, the path of least resistance isn't to pursue payment from the user of health services. No, the hospital simply bills insurers more on everything else to compensate.

The people who work, pay their taxes, and pay their premiums, (and then have to pay their absurd deductible) end up paying multiple times, for themselves and for others who are unwilling to.

We get shafted, everyone else gets to free-ride.

I will be publishing a post of how to mitigate these problems soon at Risk & Progress

I am not sure the goal is "fix" anything. Trump understands affordability is his Achilles heal. Along with recent policies such as a 10% cap on credit cards, Trump's goal is to put out policies that can easily be remembered by the voter. Now every Republican can point to this plan as a way to deflect questions around healthcare costs. Outcomes only matter on the edges.

This dynamic was seen during the election most notably in the "no tax on tips" pledge. 30 of my employees are in the Gen Z cohort. Most are part time bartenders and very liberal. All of them talked about this policy and supported it even once I explained it would have no impact on their taxes.

The memetic value of any new policy must be front and center. Dems need to learn this lesson.